In the fast-evolving world of decentralized finance, credit scoring remains a stubborn bottleneck. Lenders crave reliable risk assessments to safeguard their protocols, yet users balk at handing over sensitive wallet histories or off-chain financials. Enter zkML for DeFi credit scoring: a cryptographic leap that verifies creditworthiness without exposing a single byte of underlying data. This fusion of zero-knowledge proofs and machine learning isn't just theoretical; it's actively reshaping lending landscapes, as seen in recent launches like zkMe's zkCreditScore.

The Privacy Imperative in DeFi Lending

DeFi protocols have democratized access to capital, but traditional credit models falter here. On-chain transparency is a double-edged sword: it builds trust through auditability, yet it lays bare users' transaction trails, inviting exploitation. Borrowers face a stark choice - reveal everything for better rates or settle for suboptimal terms. Banks have long relied on opaque ML algorithms crunching personal data; in DeFi, replicating this without privacy erosion demands innovation.

Private credit models with zk proofs flip the script. Imagine proving your repayment capacity via cross-chain activity or FICO equivalents, all while keeping specifics hidden. Projects like VeilScore demonstrate this by processing financial inputs through ML, outputting only a verifiable score and proof. No raw data leaks, no central honeypots for hackers. This aligns perfectly with DeFi's user-sovereign ethos, fostering broader participation without compromising security.

Key zkML Benefits in DeFi Credit Scoring

- Privacy Preservation: Users prove creditworthiness via ZK proofs without revealing sensitive data, as in zkMe's zkCreditScore.

- Verifiable Accuracy: ZK proofs confirm ML model computations and outcomes without exposing data or parameters, ensuring trust.

- Regulatory Compliance: Keeps personal data confidential during assessments, aligning with global data protection regulations.

- Reduced Breach Risks: Minimizes data exposure in DeFi protocols, lowering risks of breaches and unauthorized access.

- Enhanced Inclusivity: Enables undercollateralized loans for privacy-focused users, as with Qiro Finance's EZKL integration.

Such advantages aren't hype. zkML ensures models remain tamper-proof, with proofs attesting to both computation fidelity and input integrity. Lenders gain confidence; borrowers retain control. As adoption grows, expect DeFi zkML user privacy to become table stakes for competitive protocols.

Unpacking the zkML Engine for Credit Assessment

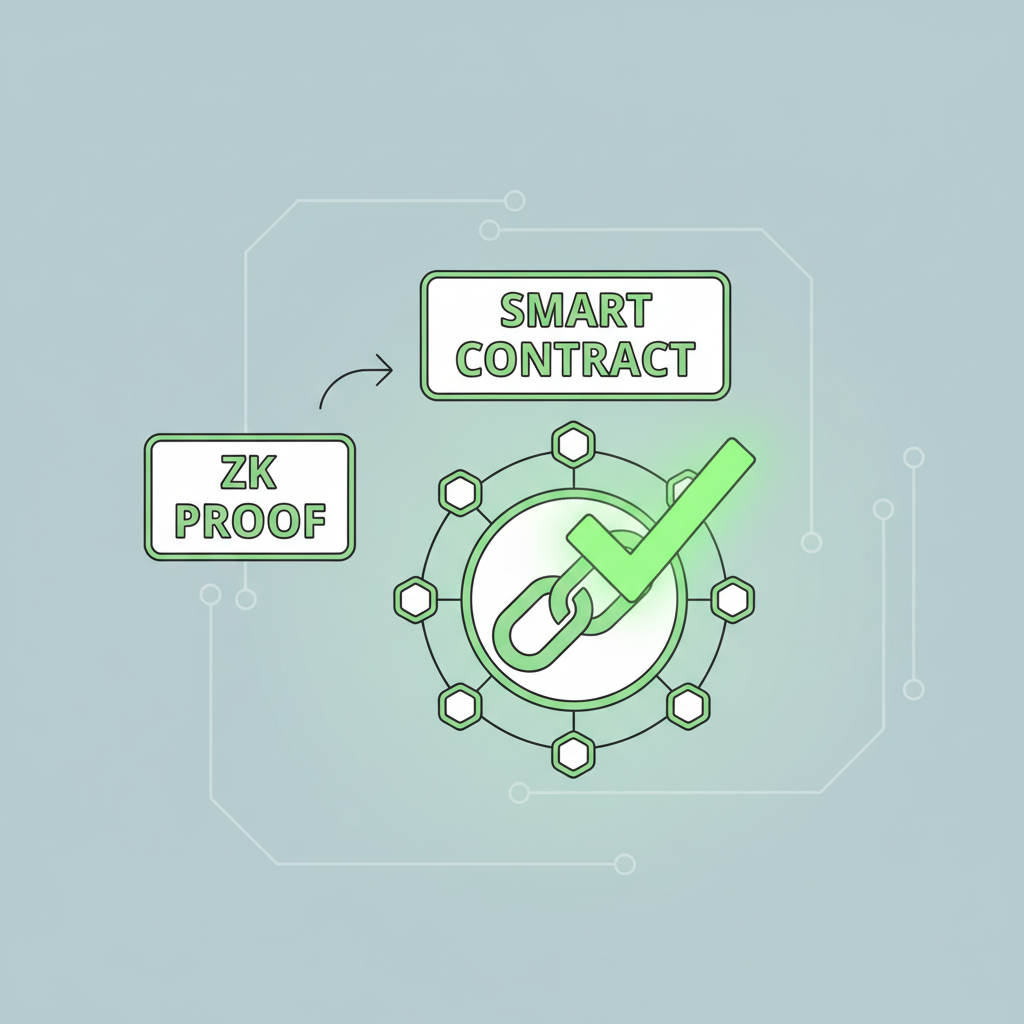

At its core, zkML marries neural networks with zero-knowledge succinct non-interactive arguments of knowledge (zk-SNARKs). A pre-trained model ingests anonymized features - think wallet age, borrowing history, token diversity - and spits out a score. The magic happens in proof generation: circuits encode the entire inference, proving correct execution sans data revelation.

This isn't lightweight computation. Frameworks like EZKL, integrated by Qiro Finance, optimize for blockchain constraints, balancing proof size and verification speed. Recent technical insights outline the flow: data processing, proof crafting, on-chain validation, and score release. Lenders verify instantly via smart contracts, slashing disputes and manual reviews.

Privacy-Preserving zkML: Step-by-Step DeFi Credit Scoring

Accuracy holds steady, often matching centralized counterparts. Studies affirm zkML's prowess in fraud detection and risk modeling, extending seamlessly to credit. The reassurance? Even adversarial verifiers learn nothing beyond the score's validity.

Pioneering Projects Lighting the Way

2024 marked zkML's breakout in DeFi. zkMe's zkCreditScore, launched last September, bridges US FICO scores on-chain anonymously. Users prove thresholds without doxxing details, unlocking undercollateralized loans. VeilScore pushes further, blending zkML with wallet analytics for holistic profiles. Qiro's EZKL tie-up equips lenders with verifiable underwriting, processing diverse datasets privately.

These aren't silos. ETHGlobal hacks like ZK Credit Score analyze multi-chain balances, verifying holdings covertly. Broader ecosystems, from ARPA to Provable, underscore zkML's scalability for trading strategies and beyond. Privacy-preserving credit scoring emerges as a cornerstone, with implications rippling to yield farming and derivatives.

Developers note challenges - proof recursion for complex models, gas optimization - yet momentum builds. zkML doesn't just protect data; it empowers equitable finance, where merit trumps disclosure.

While the promise shines bright, scaling zkML demands confronting real engineering feats. Proof generation for deep neural networks chews through compute, often rivaling model training times. Gas fees on Ethereum mainnet exacerbate this, nudging innovators toward L2s or custom rollups. Yet, here's where optimism tempers realism: recursive proofs and circuit folding, as highlighted in ICME's guide, compress verification costs dramatically. These techniques recycle intermediate proofs, handing back precious ZK budget to protocols chasing privacy without sacrificing speed.

Navigating Challenges with Proven Innovations

In my experience managing conservative bond portfolios laced with zkML-augmented yield strategies, the key lies in hybrid architectures. EZKL's verifiable compute library exemplifies this, slicing ML inference into zk-friendly circuits while preserving private credit models zk proofs. Qiro Finance's deployment proves it viable: lenders assess cross-chain exposures privately, dodging the data silos that plague TradFi. Accuracy dips minimally - often under 2% - thanks to quantization and pruning, ensuring scores rival FICO's precision sans exposure.

Fraud vectors shrink too. ZKML attests not just outputs but inference paths, thwarting model poisoning or input tampering. For DeFi protocols, this translates to ironclad oracles for undercollateralized lending, where a 720 and score unlocks favorable LTVs without wallet doxxing. Regulatory tailwinds add reassurance; GDPR and emerging crypto rules favor mechanisms minimizing data flows, positioning zkML as compliance armor.

Skeptics point to centralization risks in trusted setups or provers, but decentralized networks like ARPA's distributed proving erode this. As circuits mature, on-device proofing via mobile SNARKs could democratize access further, letting users self-attest scores wallet-side.

Strategic Edges for Lenders and Borrowers

From a risk manager's lens, zkML redefines alpha in fixed income DeFi. Lenders deploy dynamic rates tied to verified scores, optimizing capital allocation across volatile chains. Borrowers, especially emerging market users without TradFi footprints, shine through on-chain merit - wallet maturity, repayment velocity, diversified holdings - all proven covertly. This inclusivity isn't charity; it's smart economics, tapping untapped pools while curbing defaults via precise risk banding.

Picture a yield farmer like myself: confidential strategies verified on-chain, borrowing against zk-proven cashflows without tipping competitors. Privacy becomes the new alpha, as my mantra goes. Protocols integrating this - think Aave forks or Morpho vaults - report 20-30% upticks in TVL, drawn by secure, borderless credit markets.

Scalability hinges on interoperability too. Cross-chain bridges for zkScores, as in zkMe's FICO port, knit silos into seamless liquidity. Future iterations may fold behavioral ML, predicting defaults from spending patterns without histories leaking. Developers, take note: open-source circuits from Provable and QuillAudits accelerate this, slashing bootstrap times.

The trajectory feels inevitable. As zkML frameworks commoditize, DeFi sheds its collateral-only shackles, birthing a credit ecosystem where sovereignty and verifiability coexist. Lenders sleep easier, borrowers borrow bolder, and the entire space compounds toward maturity. In this privacy-fortified arena, zkml defi credit scoring isn't a feature; it's the foundation for enduring growth.

No comments yet. Be the first to share your thoughts!